Ever wondered how insurance companies determine the premiums you pay for your health insurance? Predicting insurance premiums is more than just a numbers game—it’s a task that can impact millions of lives. In this blog, we’ll demystify this complex process by walking you through an end-to-end example of predicting health insurance premium charges by demonstrating with Python code example. Specifically, we’ll use a linear regression model to predict these charges based on various factors like age, BMI, and smoking status. Whether you’re a beginner in data science or a seasoned professional, this blog will offer valuable insights into building and evaluating regression models.

Linear Regression is a supervised machine learning algorithm used for predicting a numerical dependent variable based on one or more features (independent variables). In the case of insurance, the target variable is the insurance premium (charge), and the features could be age, gender, BMI, and so on. For learning more about linear regression models, check out my other related blogs:

The following are key steps which will be explained while building the regression models for predicting health insurance premium charges:

We will work with the insurance data which can be found on this Github page – Insurance Linear Regression Model Example. The dataset contains the following columns:

First and foremost, we will load the data.

import pandas as pd

# Load the data

file_path = '/path/to/insurance.csv'

insurance_data = pd.read_csv(file_path)

# Display the first few rows

print(insurance_data.head())

Exploratory Data Analysis (EDA) is an essential step to understand the data before building any machine learning model. We’ll look into the following commonly explored aspects:

Let’s start with the descriptive statistics to get an overview of the numerical columns in the dataset.

# Generate descriptive statistics of the numerical columns

insurance_data.describe()

The descriptive statistics for the numerical columns are as follows:

Next, let’s check the data types of each column and see if there are any missing values.

# Check data types and missing values

data_info = pd.DataFrame({

'Data Type': insurance_data.dtypes,

'Missing Values': insurance_data.isnull().sum(),

'Unique Values': insurance_data.nunique()

})

data_info

The data types and missing values are as follows:

All columns have appropriate data types and there are no missing values, which is a great news. Handling missing values is a critical step in the data preprocessing pipeline, as most machine learning algorithms cannot work with missing data directly. Here are some common techniques to deal with missing values:

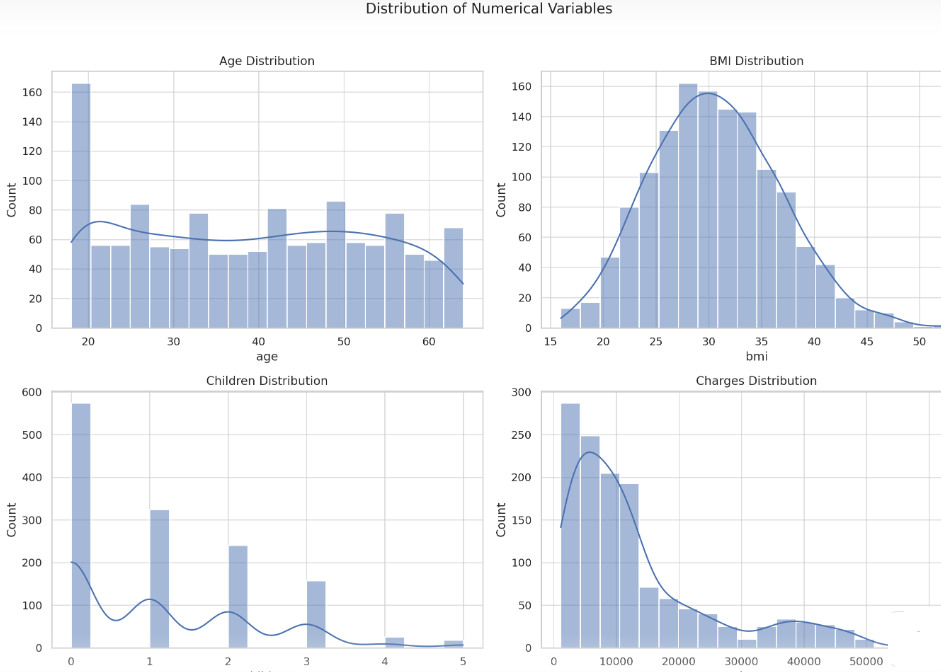

Let’s move on to the univariate analysis. We’ll start by visualizing the distribution of the numerical variables (age, bmi, children, and charges) and then take a look at the categorical variables (sex, smoker, and region).

We’ll plot histograms for age, bmi, children and charges to understand their distributions.

import matplotlib.pyplot as plt

import seaborn as sns

# Set the style for the visualizations

sns.set(style="whitegrid")

# Plot histograms for numerical variables

fig, axes = plt.subplots(2, 2, figsize=(14, 10))

fig.suptitle('Distribution of Numerical Variables')

sns.histplot(insurance_data['age'], kde=True, bins=20, ax=axes[0, 0])

axes[0, 0].set_title('Age Distribution')

sns.histplot(insurance_data['bmi'], kde=True, bins=20, ax=axes[0, 1])

axes[0, 1].set_title('BMI Distribution')

sns.histplot(insurance_data['children'], kde=True, bins=20, ax=axes[1, 0])

axes[1, 0].set_title('Children Distribution')

sns.histplot(insurance_data['charges'], kde=True, bins=20, ax=axes[1, 1])

axes[1, 1].set_title('Charges Distribution')

plt.tight_layout(rect=[0, 0, 1, 0.96])

plt.show()

Here’s what we can observe from the histograms:

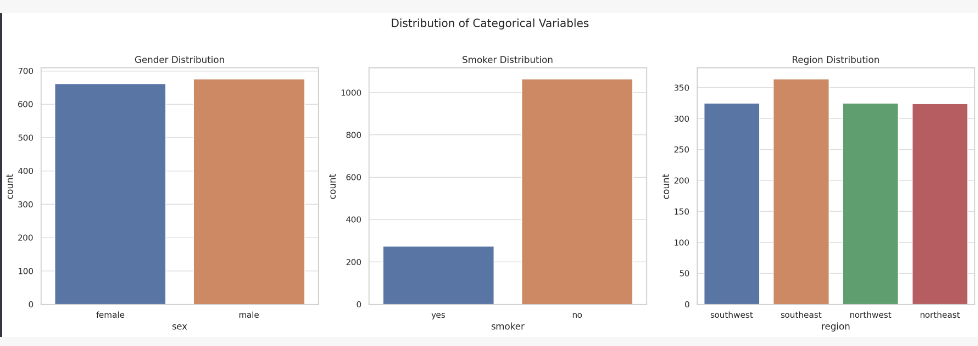

Next, let’s look at the distribution of the categorical variables (sex, smoker, and region) using bar plots.

# Plot bar plots for categorical variables

fig, axes = plt.subplots(1, 3, figsize=(18, 6))

fig.suptitle('Distribution of Categorical Variables')

sns.countplot(x='sex', data=insurance_data, ax=axes[0])

axes[0].set_title('Gender Distribution')

sns.countplot(x='smoker', data=insurance_data, ax=axes[1])

axes[1].set_title('Smoker Distribution')

sns.countplot(x='region', data=insurance_data, ax=axes[2])

axes[2].set_title('Region Distribution')

plt.tight_layout(rect=[0, 0, 1, 0.96])

plt.show()

The bar plots for the categorical variables show the following:

Now that we have a better understanding of the individual features, let’s move on to bivariate analysis to explore the relationships between these features and the target variable (charges).

In the bivariate analysis, we’ll focus on understanding the relationship between the individual features and the target variable, charges.

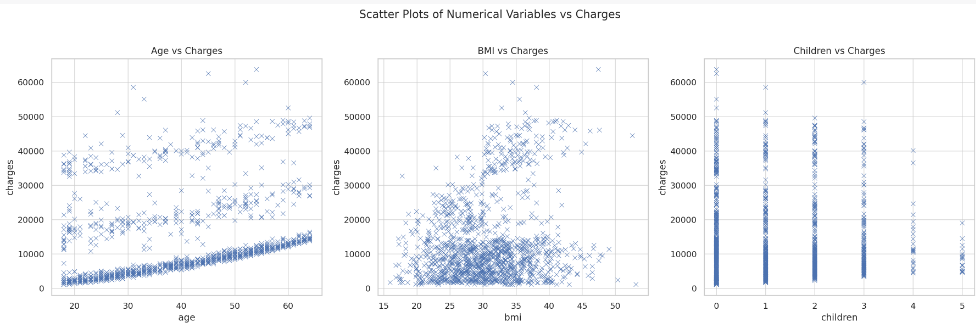

We’ll start by plotting scatter plots between the numerical variables (age, bmi, children) and charges to observe any trends or patterns.

# Plot scatter plots for numerical variables vs charges

fig, axes = plt.subplots(1, 3, figsize=(18, 6))

fig.suptitle('Scatter Plots of Numerical Variables vs Charges')

sns.scatterplot(x='age', y='charges', data=insurance_data, ax=axes[0])

axes[0].set_title('Age vs Charges')

sns.scatterplot(x='bmi', y='charges', data=insurance_data, ax=axes[1])

axes[1].set_title('BMI vs Charges')

sns.scatterplot(x='children', y='charges', data=insurance_data, ax=axes[2])

axes[2].set_title('Children vs Charges')

plt.tight_layout(rect=[0, 0, 1, 0.96])

plt.show()

Here are some observations from the scatter plots:

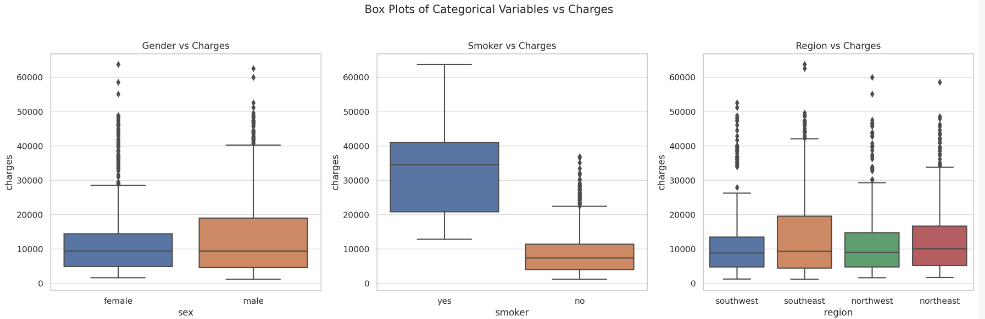

Next, let’s look at how the categorical variables (sex, smoker and region) relate to the insurance charges. We’ll use box plots for this analysis.

# Plot box plots for categorical variables vs charges

fig, axes = plt.subplots(1, 3, figsize=(18, 6))

fig.suptitle('Box Plots of Categorical Variables vs Charges')

sns.boxplot(x='sex', y='charges', data=insurance_data, ax=axes[0])

axes[0].set_title('Gender vs Charges')

sns.boxplot(x='smoker', y='charges', data=insurance_data, ax=axes[1])

axes[1].set_title('Smoker vs Charges')

sns.boxplot(x='region', y='charges', data=insurance_data, ax=axes[2])

axes[2].set_title('Region vs Charges')

plt.tight_layout(rect=[0, 0, 1, 0.96])

plt.show()

The box plots reveal the following insights:

The EDA has provided valuable insights into how various features relate to insurance charges. Now we are better equipped to build a linear regression model for predicting insurance premiums. As a next step, we will prepare data before we train the model.

Before building the model, let’s summarize our understanding of the features based on the exploratory data analysis:

Based on the above, the following is the rationale for feature selection:

The next step is data preparation for modeling, which includes encoding categorical variables and splitting the data into training and test sets.

In addition, we also split the data in training and testing set. This would be used for training the model and evaluating the model performance.

from sklearn.model_selection import train_test_split

from sklearn.preprocessing import StandardScaler, OneHotEncoder

from sklearn.compose import ColumnTransformer

# Define the features and the target

X = insurance_data.drop('charges', axis=1)

y = insurance_data['charges']

# Identify numerical and categorical columns

numerical_cols = ['age', 'bmi', 'children']

categorical_cols = ['sex', 'smoker', 'region']

# Preprocessing for numerical data: standardization

numerical_transformer = StandardScaler()

# Preprocessing for categorical data: one-hot encoding

categorical_transformer = OneHotEncoder(handle_unknown='ignore')

# Bundle preprocessing for numerical and categorical data

preprocessor = ColumnTransformer(

transformers=[

('num', numerical_transformer, numerical_cols),

('cat', categorical_transformer, categorical_cols)])

# Split data into train and test sets

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.2, random_state=0)

The next step is training the linear regression model to predict the health insurance premium charges.

from sklearn.pipeline import Pipeline

from sklearn.linear_model import LinearRegression

# Define the model

model = LinearRegression()

# Create and evaluate the pipeline

pipeline = Pipeline(steps=[('preprocessor', preprocessor),

('model', model)

])

# Fit the model using training data

pipeline.fit(X_train, y_train)

Now that the model is trained, its time to evaluate the linear regression model performance. Here is the code:

from sklearn.metrics import mean_squared_error, mean_absolute_error, r2_score

# Predict on test data

y_pred = pipeline.predict(X_test)

# Evaluate the model

mse = mean_squared_error(y_test, y_pred)

rmse = mean_squared_error(y_test, y_pred, squared=False)

mae = mean_absolute_error(y_test, y_pred)

r2 = r2_score(y_test, y_pred)

evaluation_metrics = {

'Mean Squared Error': mse,

'Root Mean Squared Error': rmse,

'Mean Absolute Error': mae,

'R-squared': r2

}

evaluation_metrics

The regression model’s performance metrics on the test set are as follows:

The following can be interpreted based on above metrics:

So, there we have it—a comprehensive guide to predicting insurance premiums using Linear Regression. From understanding the intricacies of insurance data to diving deep into exploratory data analysis, and finally building and evaluating our model, we’ve covered quite a bit of ground. But what did we really learn?

We’ve all been in that meeting. The dashboard on the boardroom screen is a sea…

When building a regression model or performing regression analysis to predict a target variable, understanding…

If you've built a "Naive" RAG pipeline, you've probably hit a wall. You've indexed your…

If you're starting with large language models, you must have heard of RAG (Retrieval-Augmented Generation).…

If you've spent any time with Python, you've likely heard the term "Pythonic." It refers…

Large language models (LLMs) have fundamentally transformed our digital landscape, powering everything from chatbots and…

{kind=link}

{kind=link}

{kind=link}

{kind=link}