Blockchain is a distributed database that allows for secure, transparent, and tamper-proof transactions. It was first introduced in 2009 as the underlying technology behind Bitcoin. Blockchain has since garnered a great deal of attention due to its potential applications in a variety of industries. In this blog post, we will explore what blockchain is and how it works!

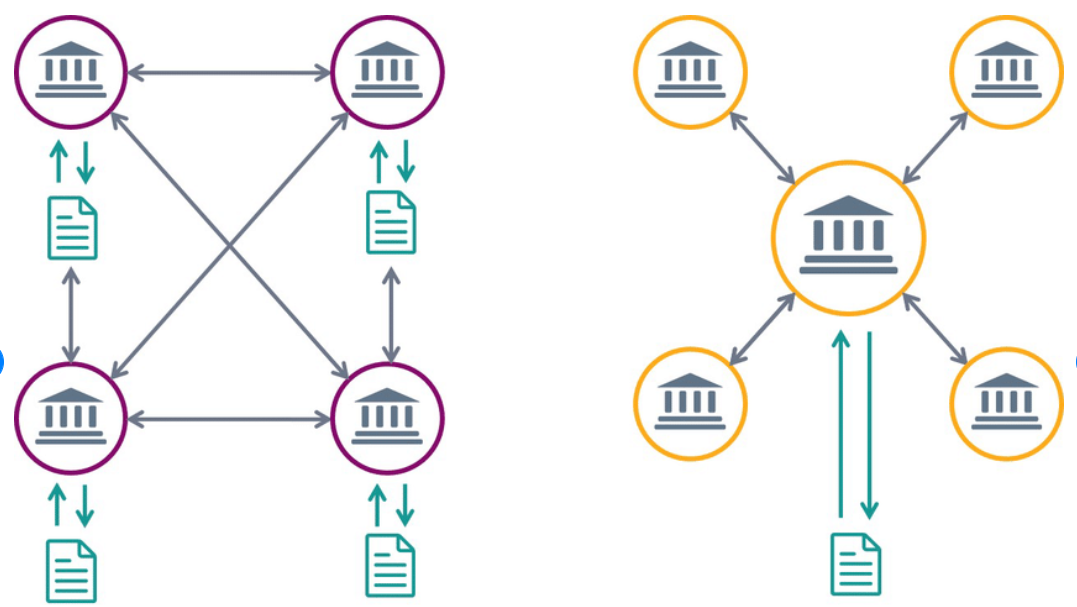

Blockchain is a distributed database that allows for secure, transparent, and tamper-proof transactions. Blockchain was originally conceived as the underlying technology for the cryptocurrency bitcoin. However, Blockchain has since been found to have many other potential use cases. The key concepts behind Blockchain are decentralization, immutability, and consensus. Blockchain transactions are verified by a network of computers rather than a central authority, making it more resistant to fraud and tampering. The decentralized nature of Blockchain also makes it more secure, as there is no single point of failure. The picture below represents the decentralized aspect of Blockchain (left image) rather than the traditional way of storing the transactions (Centralized).

Blockchain records are immutable, meaning they cannot be altered or deleted, ensuring that transaction histories are complete and accurate. Finally, Blockchain networks reach a consensus on the valid state of the ledger through a process known as mining. Miners compete to solve complex mathematical problems in order to validate transactions and add new blocks to the chain. In return for their work, miners are rewarded with cryptocurrency.

The first and most well-known type of blockchain is the Bitcoin blockchain, which powers the Bitcoin cryptocurrency. However, there are many other types of blockchain that have been developed for different purposes. For example, Ethereum is a blockchain that can be used to create and run decentralized applications. Ripple is a blockchain that is designed for fast and efficient international payments. There are also private and permissioned blockchains, which are designed for use within specific organizations. Each type of blockchain has its own unique features and characteristics, but all share the same core concepts of decentralization, security, and transparency.

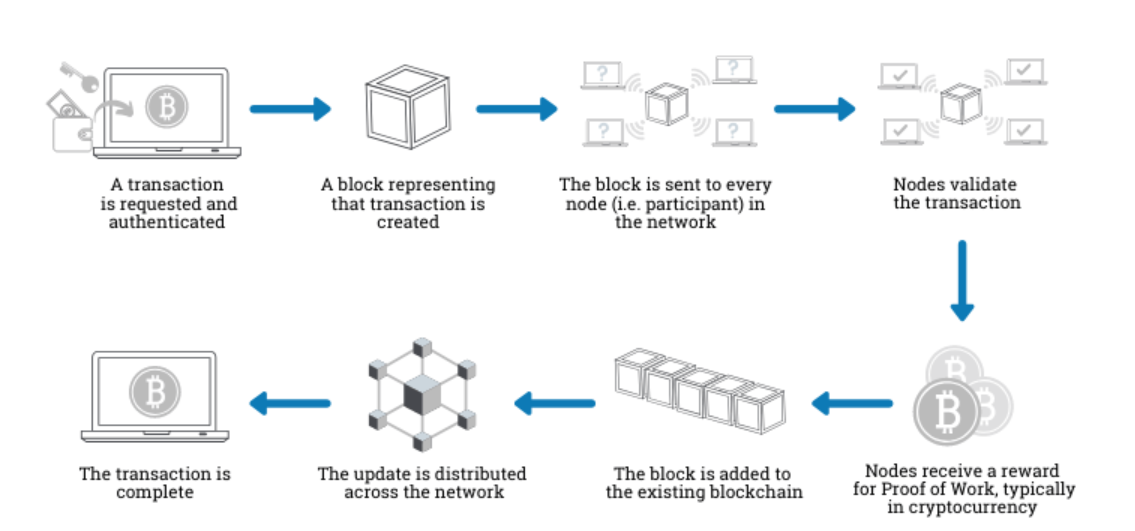

Now that we have a basic understanding of Blockchain, let’s take a look at how it works. Blockchain transactions are grouped into blocks, which are then chained together. Each block contains a cryptographic hash of the previous block, a timestamp, and transaction data. The chain is stored across a network of computers, known as nodes. In order for a transaction to be added to the Blockchain, it must be verified by the nodes in the network. Once verified, the transaction is added to a block, which is then broadcasted to the network. The new block is then added to the Blockchain and propagated across the network. Miners play an important role in this process, as they validate transactions and add new blocks to the Blockchain. In return for their work, miners are rewarded with cryptocurrency. The picture given below represents how does a transaction gets stored in the blockchain:

The following are three different types of Blockchain:

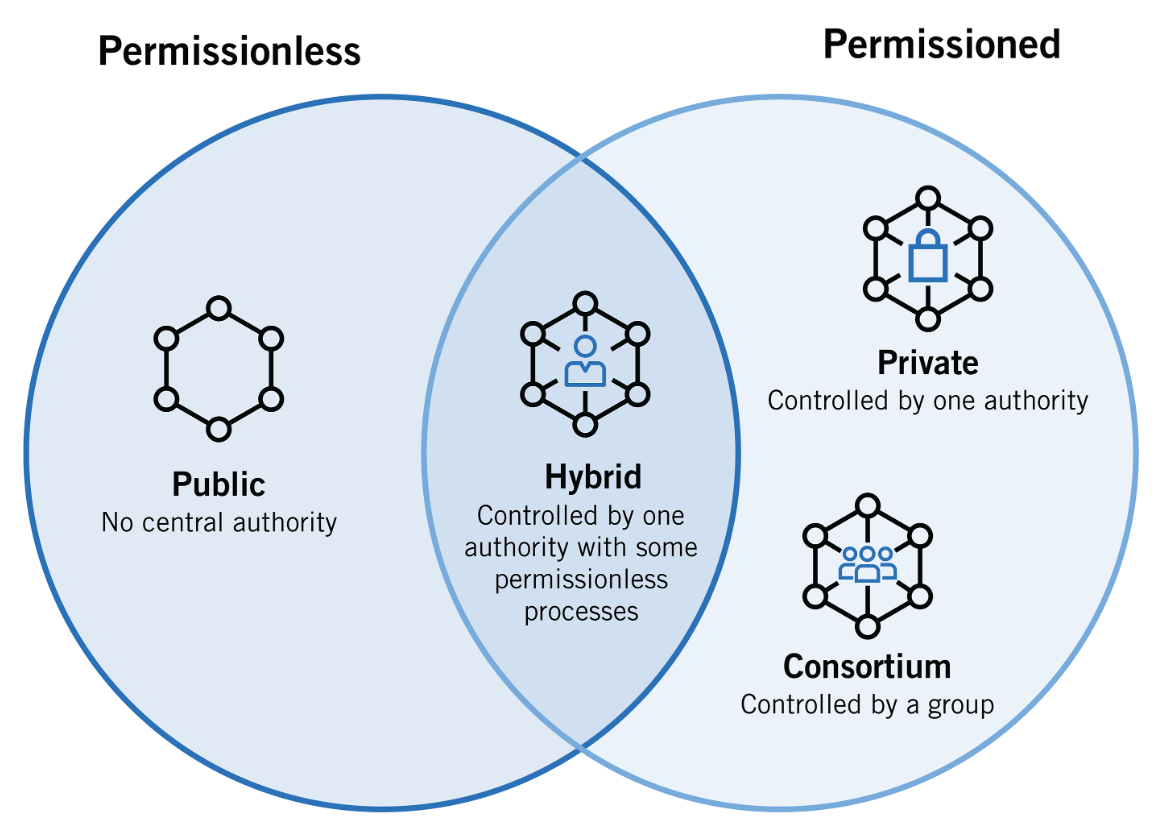

The picture below represents different types of blockchains including public, private, and hybrid blockchain.

There are many blockchain frameworks available that can be used for blockchain development. Some of the most popular blockchain frameworks include Hyperledger Fabric, Ethereum, Corda, and Multichain. Each blockchain framework has its own set of features and benefits. The following is the detail:

The above-mentioned frameworks are just a few examples of blockchain frameworks that can be used for developing blockchain applications. The best way to determine which blockchain framework is right for a particular project is to consult with a blockchain development expert.

Blockchain is a rapidly emerging technology with the potential to revolutionize a wide range of industries. While Blockchain holds great promise, it also presents a unique set of challenges. As a result, Blockchain projects often require a specific set of skills and expertise.

First and foremost, Blockchain projects require individuals with a strong foundation in mathematics and computer science. This is essential for understanding how Blockchain works and for developing new applications. In addition, Blockchain projects often require experience with distributed systems and distributed ledger technologies. Individuals with this expertise can help to ensure that Blockchain projects are secure and efficient. Finally, Blockchain projects often involve complex financial transactions. As a result, individuals with experience in finance and accounting can be extremely valuable to Blockchain teams.

Blockchain is an emerging and promising technology. The blockchain framework can be used for developing blockchain applications that are secure, transparent, and tamper-proof. Blockchain frameworks vary in their features but the most important feature to look out for when choosing a framework is its scalability – since transactions on Blockchain will increase over time with more users joining the network, it’s essential that your chosen Blockchain has enough nodes available so as not to congest or slow down the system due to lack of bandwidth capabilities. We hope this article helped you understand what Blockchain really means and how it works! If you have any questions about Blockchain development feel free to drop a message below and I will reach out to you.

We’ve all been in that meeting. The dashboard on the boardroom screen is a sea…

When building a regression model or performing regression analysis to predict a target variable, understanding…

If you've built a "Naive" RAG pipeline, you've probably hit a wall. You've indexed your…

If you're starting with large language models, you must have heard of RAG (Retrieval-Augmented Generation).…

If you've spent any time with Python, you've likely heard the term "Pythonic." It refers…

Large language models (LLMs) have fundamentally transformed our digital landscape, powering everything from chatbots and…

{kind=link}

{kind=link}

{kind=link}